How to Optimize Your Investing with Tax Strategies

Optimize your portfolio with investing tax strategies. Learn techniques to boost returns and enhance financial growth by leveraging smart tax planning.

Retirement and tax planning go hand in hand, yet many overlook this critical connection. At Sager CPA, we’ve seen firsthand how proper planning can significantly impact your financial well-being during retirement.

This blog post will guide you through the essential tax considerations for your golden years, from understanding different retirement accounts to optimizing Social Security benefits. We’ll also share strategies to minimize your tax burden and maximize your retirement income.

Traditional IRAs provide immediate tax benefits. Everyone is eligible to make contributions to a traditional IRA, but a tax deduction for those contributions may not always be available. However, you pay taxes on withdrawals in retirement. This option works well if you expect a lower tax bracket when you retire.

Roth IRAs offer no immediate tax break. You make contributions with after-tax dollars. The major advantage? Qualified withdrawals in retirement incur no taxes. Roth IRAs have fewer restrictions, but fewer tax breaks as well. This can significantly benefit you if you anticipate a higher tax bracket in retirement or if tax rates increase in the future.

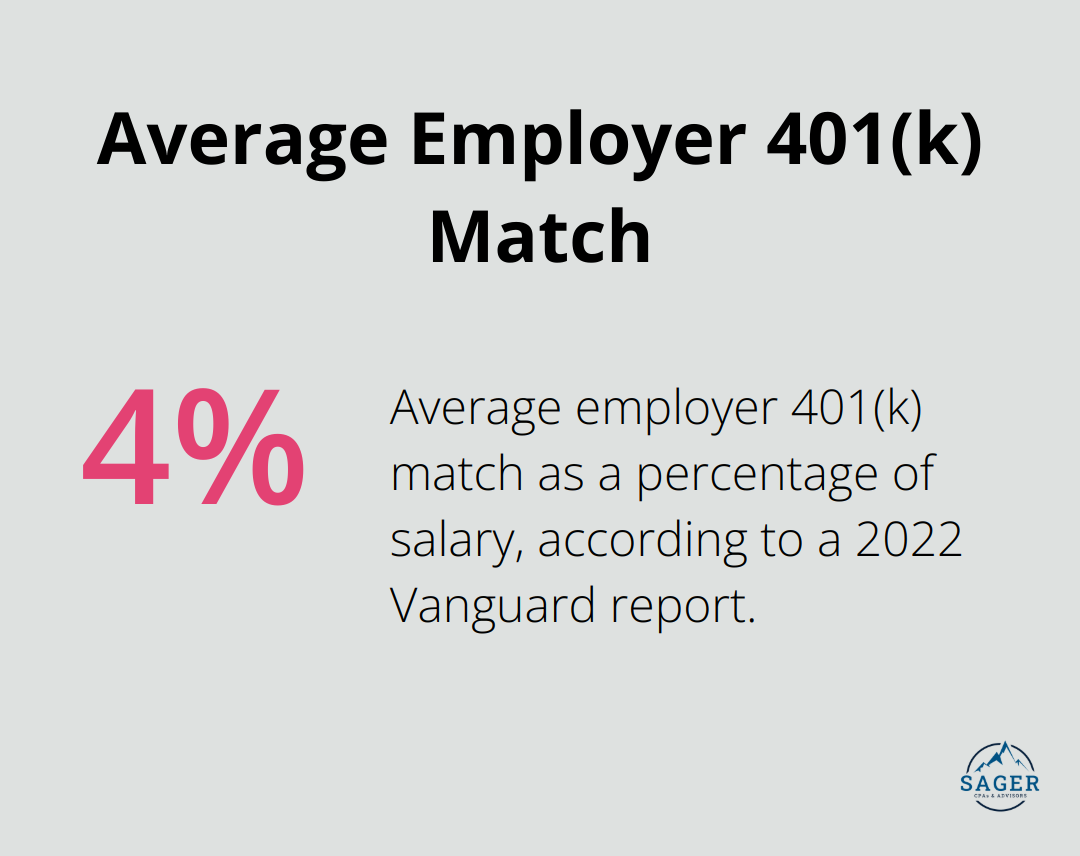

401(k) plans, typically offered by employers, allow pre-tax dollar contributions, similar to traditional IRAs. Many employers offer matching contributions (essentially free money). A 2022 Vanguard report shows the average employer match at 4.5% of salary. This can substantially increase your retirement savings while reducing your current tax bill.

However, like traditional IRAs, you owe taxes on withdrawals in retirement. You must factor this future tax liability into your retirement planning.

For self-employed individuals or small business owners, SEP IRAs and Solo 401(k)s offer higher contribution limits compared to traditional IRAs. In 2023, you can contribute up to $22,500 to a 401(k) if you’re under 50, with catch-up contributions available for those 50 and older.

These accounts function similarly to traditional IRAs and 401(k)s from a tax perspective. Contributions reduce your current taxable income, but withdrawals in retirement count as ordinary income for tax purposes.

Your choice of retirement account significantly affects your tax strategy. Each account type has unique rules and potential benefits. The best choice depends on your individual circumstances, current tax situation, and future expectations.

For example, if you expect your income (and tax rate) to increase substantially in the future, a Roth IRA might prove more beneficial. On the other hand, if you’re in a high tax bracket now and anticipate lower income in retirement, a traditional IRA or 401(k) could offer more advantages.

It’s also worth considering a mix of account types to provide tax diversification in retirement. This strategy allows you to manage your tax liability more effectively by choosing which accounts to withdraw from each year.

Understanding these tax implications forms a critical part of effective retirement planning. The right strategy can save you thousands of dollars in taxes over your lifetime. As we move forward, we’ll explore strategies to minimize taxes in retirement, helping you make the most of your hard-earned savings.

Retirement doesn’t signal the end of tax planning. It’s a prime time to implement smart strategies that can significantly reduce your tax burden. Here are some effective approaches to consider:

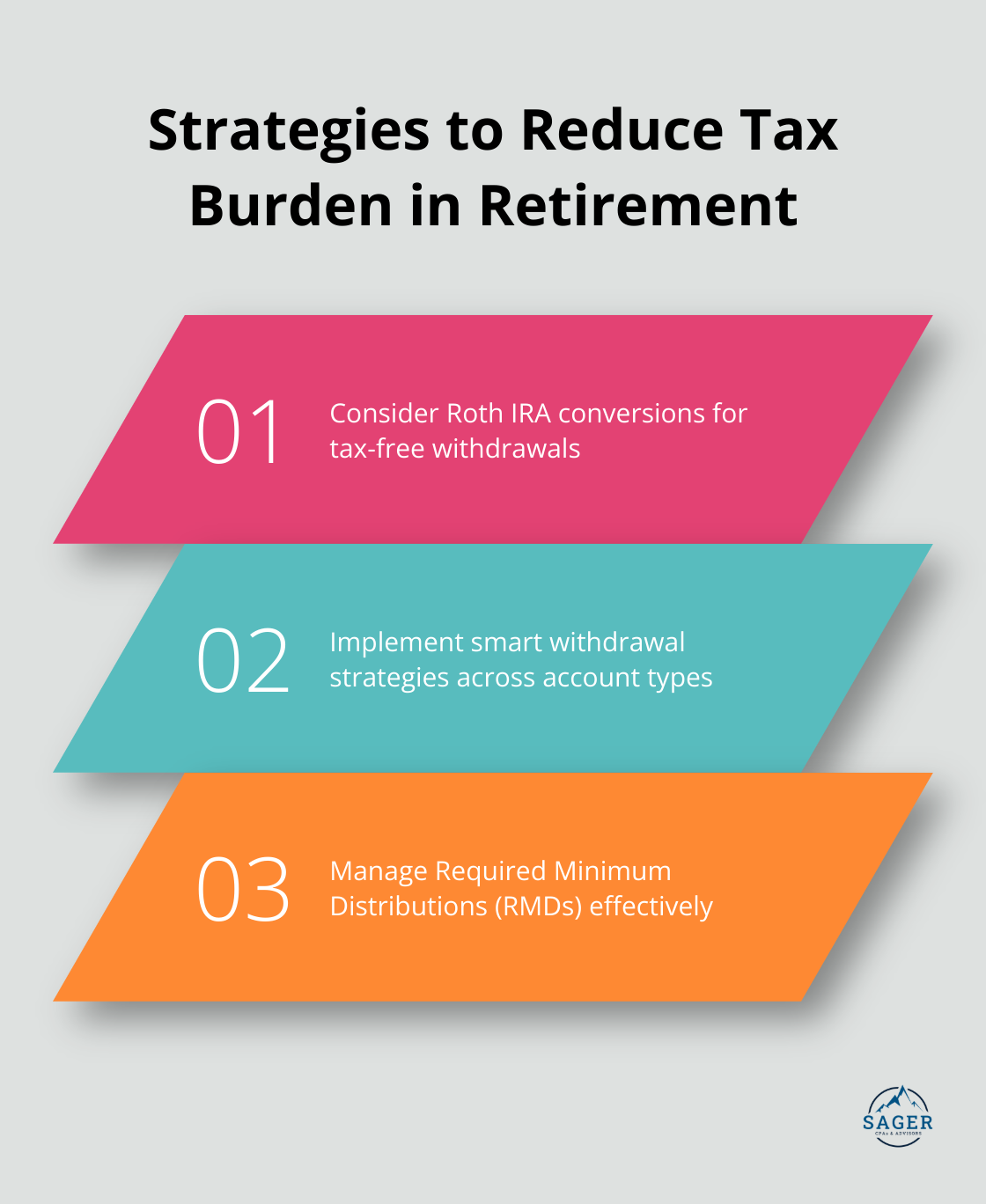

A Roth conversion involves moving money from a traditional IRA to a Roth IRA. One of the biggest advantages of a Roth IRA conversion is the ability to enjoy tax-free withdrawals in retirement. This strategy can benefit you if you expect to be in a higher tax bracket in retirement or if you believe tax rates will increase in the future.

The ideal time for a Roth conversion is often in years when your income is lower, such as early retirement before you start collecting Social Security. This approach can help you avoid pushing yourself into a higher tax bracket during the conversion.

The order in which you withdraw from your retirement accounts can significantly impact your tax bill. A common strategy starts with taxable accounts, then moves to tax-deferred accounts (like traditional IRAs), and finally to tax-free accounts (like Roth IRAs).

However, this isn’t a one-size-fits-all solution. In some cases, it might make sense to withdraw from multiple account types each year to stay in a lower tax bracket. For instance, you might take some money from your traditional IRA up to the top of your current tax bracket, then switch to your Roth IRA for additional funds.

Once you reach age 72, you must start taking RMDs from most retirement accounts. These distributions are taxed as ordinary income and can potentially push you into a higher tax bracket.

One strategy to manage RMDs is to start withdrawing from your retirement accounts before you’re required to. This can help reduce the account balance and, consequently, lower your future RMDs.

Another approach uses your RMD to make charitable contributions through a Qualified Charitable Distribution (QCD). This allows you to satisfy your RMD requirement without increasing your taxable income.

Tax laws are complex and constantly changing. What works best for one person might not be ideal for another. That’s why it’s essential to work with experienced professionals who can tailor these strategies to your unique situation.

A skilled tax advisor can help you navigate these complexities and create a personalized tax strategy. They can assist you in identifying the most beneficial approaches for your specific circumstances, potentially saving you thousands of dollars in taxes over your retirement years.

As we move forward, let’s explore how Social Security and Medicare fit into your retirement tax planning puzzle. These programs play a significant role in your retirement income and expenses, and understanding their tax implications is key to a comprehensive retirement strategy.

The age at which you start to claim Social Security benefits affects both your benefit amount and your tax situation. If you claim benefits at age 62, your monthly payments will be lower, but you’ll receive them for a longer period. Waiting until your full retirement age (between 66 and 67, depending on your birth year) or up to age 70 can increase your monthly benefit by up to 8% per year.

From a tax perspective, delaying benefits can prove advantageous. If you’re still working or have other substantial income sources, claiming Social Security early might push you into a higher tax bracket. Waiting can potentially reduce your overall tax burden in the early years of retirement.

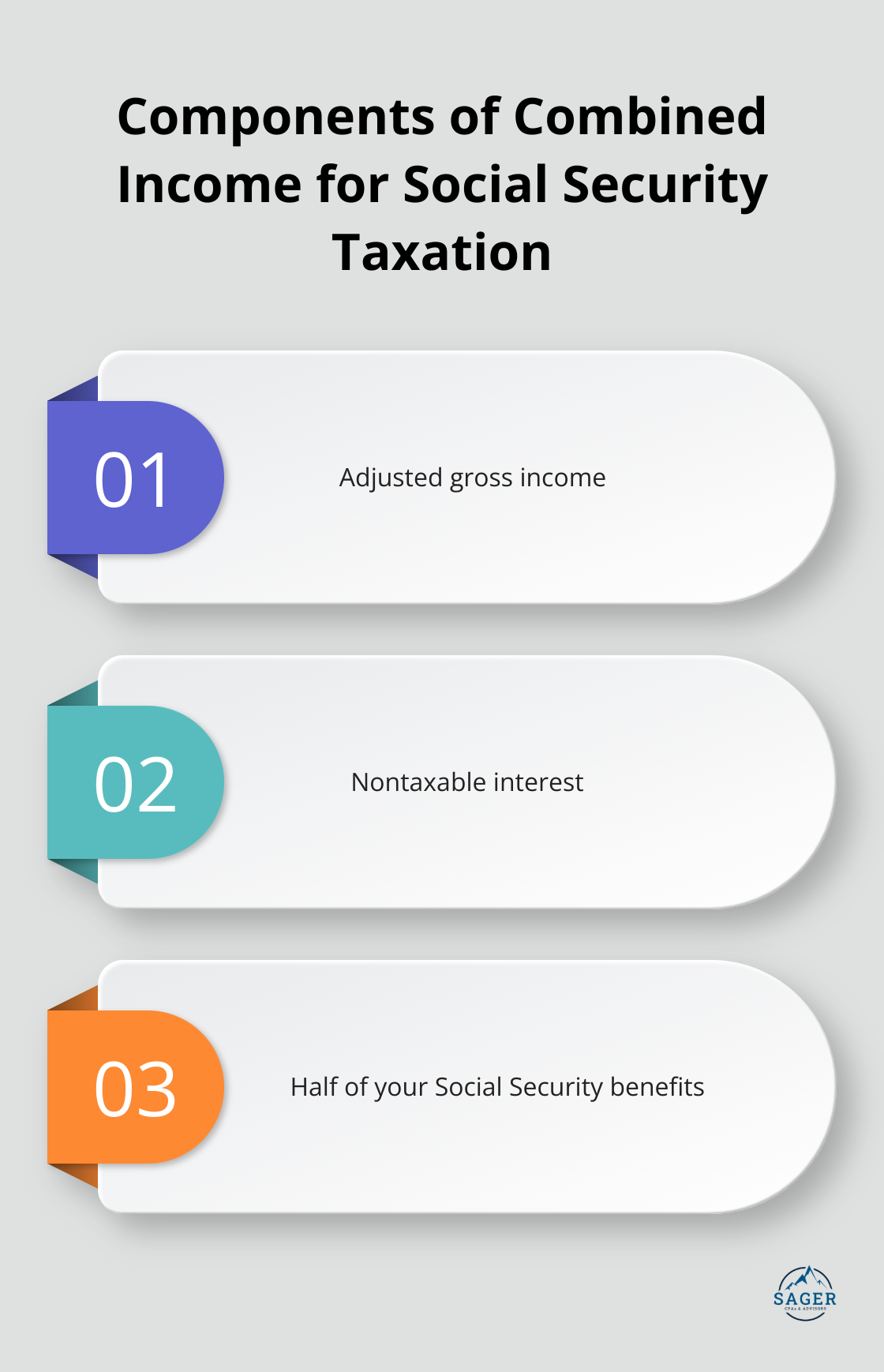

Many retirees don’t realize that their Social Security benefits may be taxable. The IRS uses a formula called “combined income” to determine if your benefits are subject to taxation. Combined income is the sum of your adjusted gross income, nontaxable interest, and half of your Social Security benefits.

To determine if their benefits are taxable, taxpayers should take half of the Social Security money they collected during the year and add it to their other income. This includes pensions, wages, interest, dividends and capital gains.

Medicare provides essential health coverage for retirees, but it’s not free. Most people don’t pay a premium for Medicare Part A, but Part B premiums are deducted from your Social Security benefits.

High-income retirees may face additional costs. If your modified adjusted gross income (MAGI) from two years prior exceeds certain thresholds, you’ll pay an Income-Related Monthly Adjustment Amount (IRMAA) on top of your standard premiums. The IRMAA sliding scale is a set of statutory percentage-based tables used to adjust Medicare Part B and Part D prescription drug coverage premiums.

To manage these costs, you can consider tax-efficient withdrawal strategies that keep your MAGI below the IRMAA thresholds. This might involve careful planning of Roth conversions, capital gains realizations, and required minimum distributions from traditional retirement accounts.

Tax laws are complex and constantly changing. What works best for one person might not be ideal for another. That’s why it’s essential to work with experienced professionals who can tailor these strategies to your unique situation.

A skilled tax advisor can help you navigate these complexities and create a personalized tax strategy. They can assist you in identifying the most beneficial approaches for your specific circumstances.

Retirement and tax planning require careful consideration and strategic decision-making. Your unique financial situation, goals, and expectations should shape your strategy. What works for one retiree may not be the best approach for another.

Sager CPA specializes in creating tailored financial strategies that optimize retirement outcomes. Our team of experts can help you navigate the complexities of tax laws, retirement account options, and Social Security benefits. We provide comprehensive tax planning services to minimize your liabilities and maximize your savings.

Take control of your financial future. Implement smart tax planning strategies and seek professional guidance. Schedule a consultation with Sager CPA today to start creating your personalized retirement and tax planning strategy.

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.