How to Optimize Tax Planning for Your LLC

Optimize tax planning for your LLC with these practical tips for reducing liabilities, maximizing deductions, and making informed financial decisions.

Tax reduction strategies can significantly impact your financial well-being. At Sager CPA, we understand the importance of keeping more of your hard-earned money.

This blog post will guide you through effective methods to lower your tax burden legally and ethically. We’ll explore key areas such as deductions, credits, retirement accounts, and strategic timing of income and expenses.

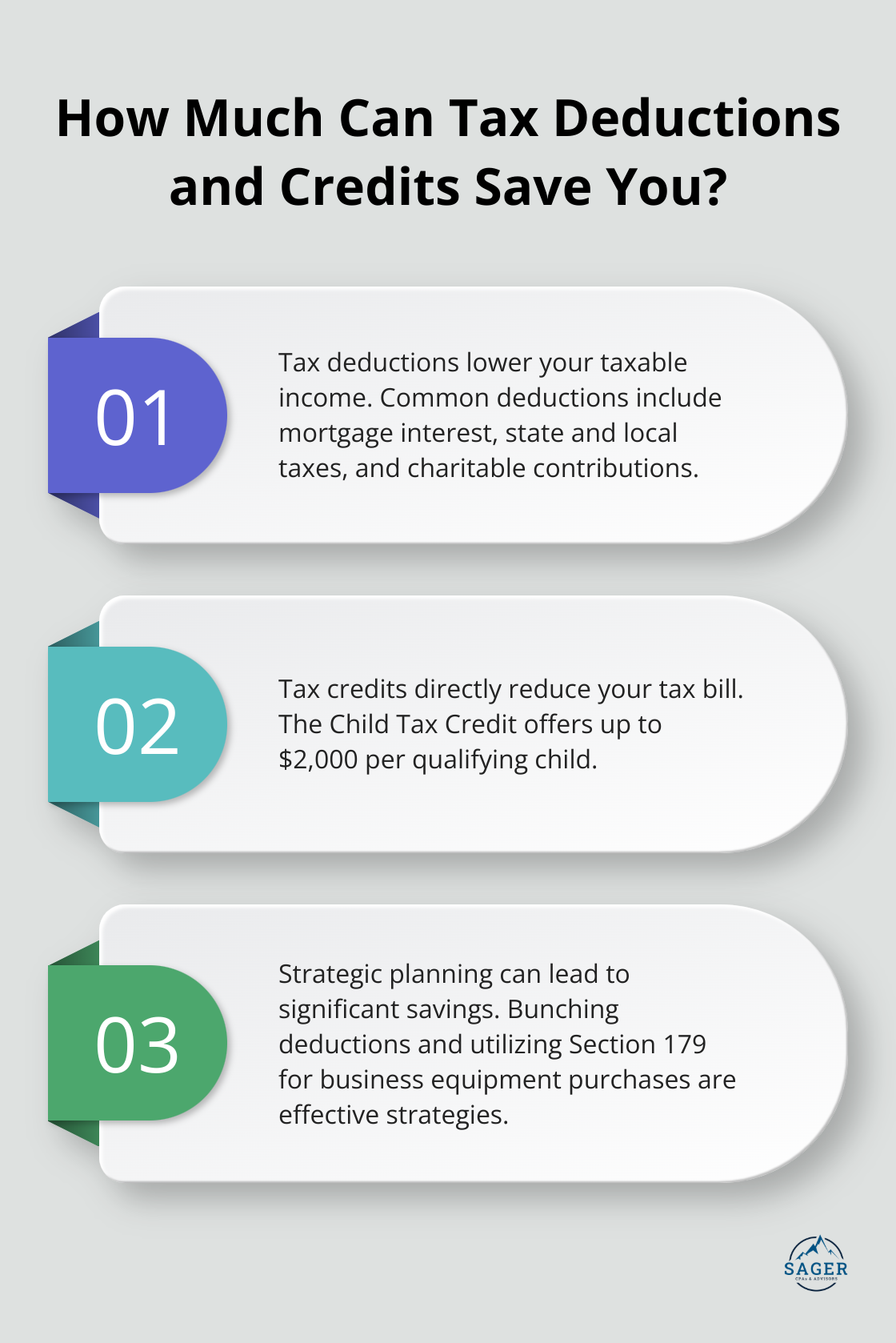

Tax deductions decrease your taxable income. At Sager CPA, we help our clients understand these concepts to maximize their tax savings.

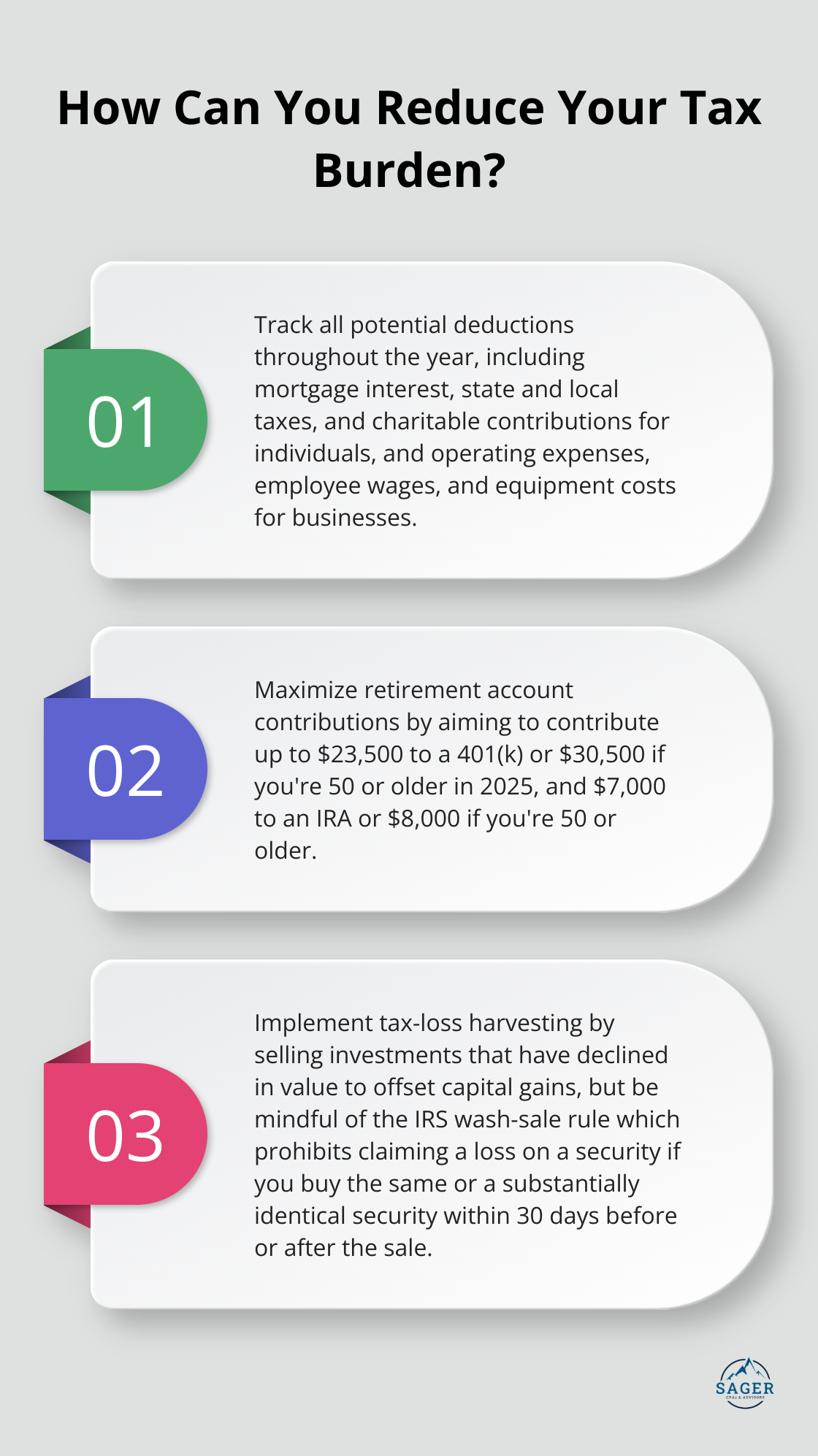

Tax deductions decrease your taxable income. Common deductions for individuals include:

Businesses can deduct:

Tax credits provide a dollar-for-dollar reduction of your tax bill. For example, a $1,000 credit will reduce a $5,000 tax bill to $4,000.

Popular credits include:

To maximize your tax savings, you must know which deductions and credits apply to your situation. Here are practical steps to take:

Tax laws change frequently. What applied last year might not apply this year. Working with experienced professionals who stay current on tax code changes is essential.

Strategic tax planning can lead to substantial savings. Consider these strategies:

These strategies can potentially save you thousands in taxes. However, their effectiveness depends on your specific financial situation.

While understanding tax deductions and credits is valuable, navigating the complex tax landscape requires expertise. A professional tax advisor can:

Now that we’ve covered the basics of tax deductions and credits, let’s explore how maximizing your retirement account contributions can further reduce your tax burden.

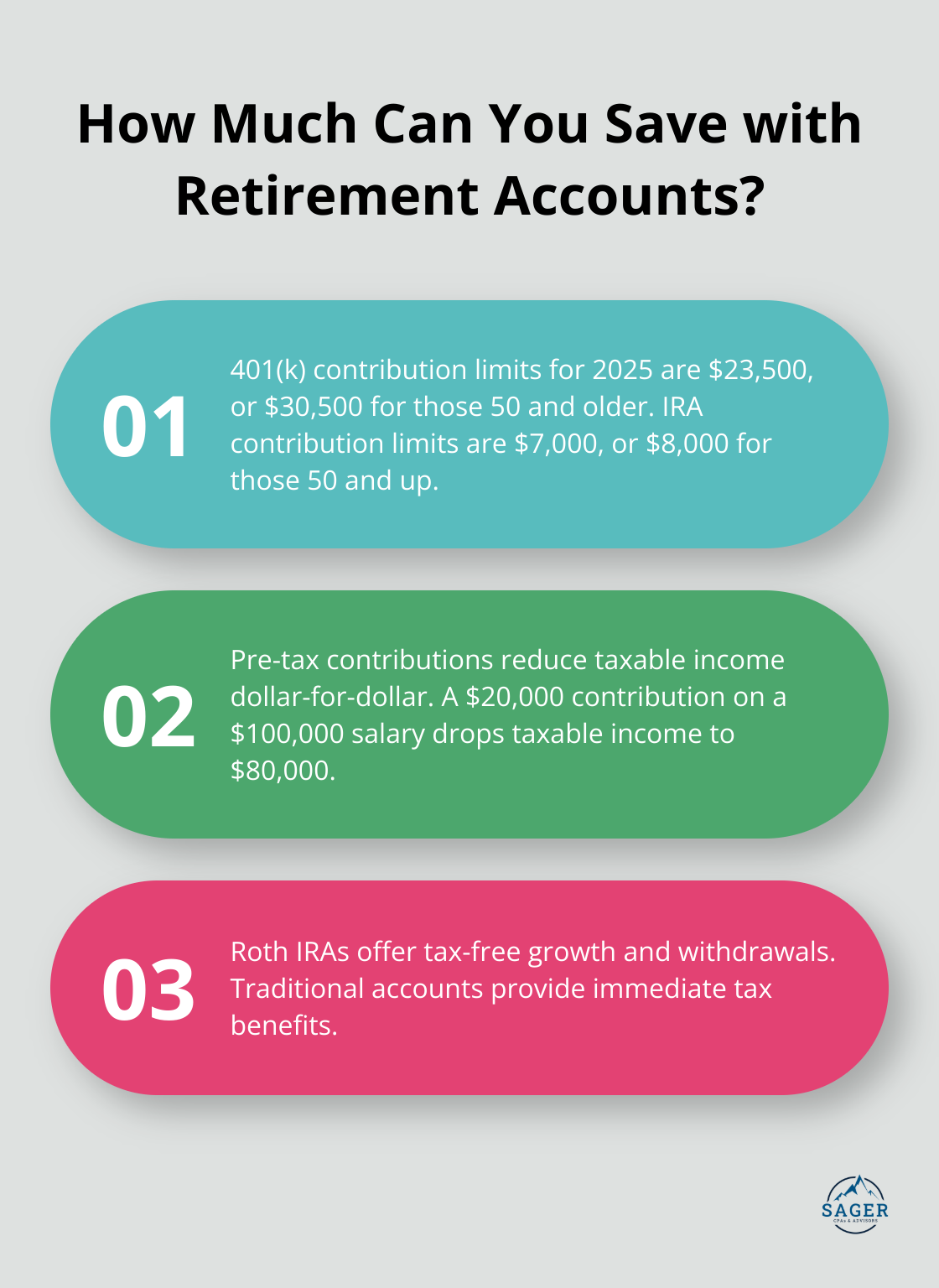

Retirement accounts serve as potent tools for tax reduction while securing your financial future. Holding some of your retirement savings in Roth accounts can help you limit how much income tax you’ll owe in a given year. In 2025, you can contribute up to $23,500 to a 401(k), or $30,500 if you’re 50 or older. For IRAs, the limit stands at $7,000, or $8,000 for those 50 and up.

These contributions, made with pre-tax dollars, reduce your taxable income dollar-for-dollar. For instance, if you earn $100,000 and contribute $20,000 to your 401(k), your taxable income drops to $80,000. This reduction can potentially move you into a lower tax bracket, further decreasing your tax bill.

The decision between Roth and traditional retirement accounts hinges on your current and expected future tax situation. Roth IRAs offer tax-free growth and withdrawals, making them appealing if you anticipate being in a higher tax bracket in retirement. Traditional accounts offer immediate tax benefits, while Roth accounts provide tax-free withdrawals in retirement.

Many individuals find that a mix of both Roth and traditional accounts provides the most flexibility for tax planning in retirement.

To fully leverage the tax benefits of retirement accounts, try to contribute the maximum amount allowed. If your employer offers a 401(k) match, contribute at least enough to get the full match – it’s essentially free money.

For those 50 and older, take advantage of catch-up contributions. These allow you to contribute an additional $7,500 to your 401(k) and $1,000 to your IRA in 2025, providing extra tax savings and boosting your retirement savings.

The key to maximizing these benefits lies in consistency. Regular, substantial contributions over time not only reduce your current tax bill but also set you up for a more comfortable retirement.

Now that we’ve explored how retirement accounts can significantly impact your tax situation, let’s turn our attention to another powerful strategy: the strategic timing of income and expenses.

Income deferral can significantly reduce your tax burden. This strategy involves pushing income into the next tax year to potentially lower your current year’s tax bracket. Self-employed individuals can delay billing clients until late December, ensuring payment arrives in January. Employees might request their employer to defer a year-end bonus to January. However, you must consider your expected income for both years to ensure this strategy benefits you overall.

While income deferral pushes earnings into the future, deduction acceleration brings tax relief forward. This approach involves paying for deductible expenses in the current year, even if they’re not due until the next. You could pay your January mortgage payment in December to claim the interest deduction in the current year. Similarly, making charitable donations before year-end can provide immediate tax benefits.

Businesses can take advantage of this strategy by purchasing necessary equipment or supplies in December rather than waiting until January. The Section 179 deduction allows business taxpayers to deduct the cost of certain property as an expense when the property is first placed in service.

Tax-loss harvesting is a sophisticated strategy for investment portfolios. It involves selling investments that have declined in value to realize losses, which can then offset capital gains from other investments. For example, you can use the value of your loss from industrial shares to offset the taxable gains from the sale of your tech shares, thereby reducing your overall tax liability.

The IRS wash-sale rule prohibits claiming a loss on a security if you buy the same or a “substantially identical” security within 30 days before or after the sale. Therefore, timing and selection of replacement investments are critical.

These strategies require a deep understanding of tax laws and your specific financial situation. While these techniques can lead to significant tax savings, they should be part of a comprehensive financial plan. Professional tax advisors, such as those at Sager CPA, can help develop tailored strategies that align with your overall financial goals and maximize your tax savings.

Effective tax reduction strategies can significantly impact your financial well-being. You can potentially save thousands of dollars each year by understanding and leveraging tax deductions, credits, retirement account contributions, and strategic timing of income and expenses. These approaches reduce your current tax burden and contribute to long-term financial stability and growth.

Tax laws are complex and constantly changing. You must stay informed about these changes to take advantage of all available opportunities for tax savings. What worked last year might not be the best approach this year, which makes it essential to review and adjust your tax strategies regularly.

Professional guidance becomes invaluable when navigating the intricacies of tax planning. Working with experienced tax advisors, like those at Sager CPA, can help you develop a comprehensive tax reduction strategy tailored to your unique financial situation. Their expertise in accounting, business advisory, and tax planning can provide you with the insights and support needed to make informed financial decisions and maximize your tax savings.

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.